![<?echo $_SERVER['SERVER_NAME'];?>](/template/twentyseventeen/skin/images/header.jpg)

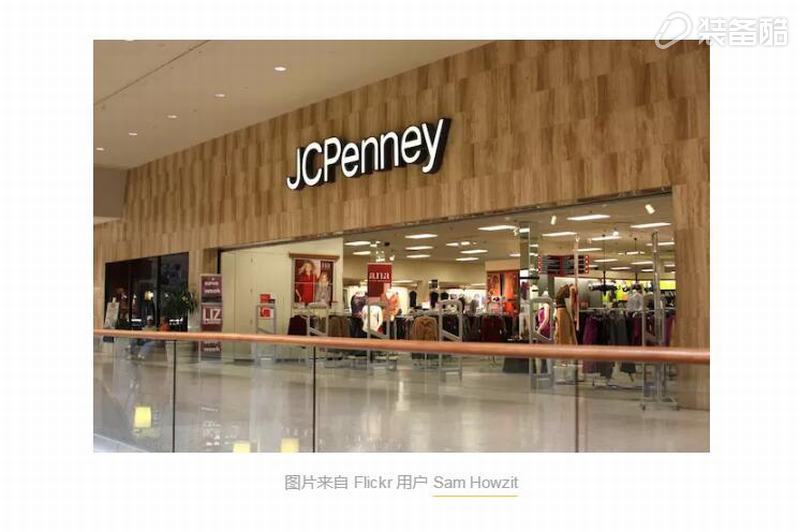

JCPenney, a department store with more than 1,000 stores in the United States, announced this week that it will set up a Nike-branded "shop-in-shop" in about 600 stores.

The so-called “store-in-shop†concept is actually corresponding to the general counter of a department store. Take Nike’s example, the “shop-in-shop†area in JCPenney has a maximum area of ​​about 46 square meters, although it is less than a hundred. Even the thousands of square meters of Nike independent stores, but with the past forced Nike department store counters have significantly improved. The most important is the visual "upgrade", "more prominent image expression, upgraded hardware, models, and a huge Nike logo on the ceiling." The independence of the entire space will be slightly stronger.

From the perspective of product supply, Nike will also provide a richer product line in the JCPenney “shop-in-shop†covering clothing, sports shoes and accessories, mainly men's products.

Although the size of the store is not large, 600 is not a small number anyway. In China, it's equivalent to Nike doing an "image escalation" in almost all major department stores you know.

This news appeared when the overall growth of Nike's performance was slow, and the so-called "slow" was also compared with competitors. Throughout the 2016 fiscal year and the latest quarter after entering FY2017, Nike’s revenue growth remained at around 6%, while Adidas’ revenue increased by 20% in the first three quarters of 2016, with Under Armour continuing for 26 consecutive years. Quarterly revenue increased by more than 20%.

Although the U.S. department store industry is sluggish today—Messy Department Store, the largest U.S. department store, lays off employees for four consecutive years after the Christmas shopping season. Just one week ago, it announced the layoff of 10,000 people. Another department store, Sears, closed in 235 in 2015 alone. Home stores, but for brands such as Nike, in the United States, "wholesale channels" from department stores, etc. contribute more than 72% to its revenue. "Wholesale channels" correspond to brand direct retail stores, which include department stores and multi-brand sporting goods stores.

Nike's intention to open stores in JCPenney (who had tried this practice in 2016) occurred eight months after competitors Under Armour announced their cooperation with another US department store, Kohl's. Under the latter agreement reached at the time, Under Armour will enter Kohl's more than 1,100 stores in the US from March this year.

However, unlike Under Armour's cooperation with Kohl's, Under Armour chose Kohl's because its main consumers are middle-class women in the suburbs of the United States. This is the consumer group that the former is currently undergoing radical expansion, and Nike’s shop-in-shop is established. In JCPenney's men's area, some stores will have a women's and children's product line.

For Nike, appearing in a department store with a more vivid image helps establish a brand image. The reason why it chose to aggravate its layout in department stores at this time is that another important wholesaler channel—the multi-brand sporting goods store—has been relying on for a long period of rest.

Sports Authority, once the nation’s largest sporting goods chain, closed more than 400 stores in the United States in early 2016 and applied for bankruptcy protection. Another similar store, City Sports, filed for bankruptcy protection at the end of 2015, which means risk for brands like Nike. .

At the same time, Fortune quoted a report from NPD as pointing out that sales of sports goods in department stores increased by 5% year-on-year, while sales at sporting goods stores were negative. In other words, in comparison, the demand for sports products from department store consumers is increasing, which is a worthy business for Nike.

However, in the long run, Nike will shift more energy to direct retail stores. According to Nike CEO Mark Parker, in November last year, Nike’s direct-to-consumer business (DTC, including official e-commerce business) is expected to reach US$16 billion by 2020, accounting for 1/3 of the company’s total revenue. The current market in the United States is about 27%.

As to why the proportion of direct-operated stores should be strengthened, Huang Xiangyan, Senior Communications Director of Nike Greater China, said in an interview with Curiosity Daily last year that this is to better convey brand image to consumers and enhance offline shopping experience. At the same time, it provides demonstrations for dealers (ie, department stores, multi-brand sports shops, etc.).

From a certain point of view, Nike's move into JCPenney this time is more like an expedient measure. On the one hand, department stores are still an important sales channel (although their influence is declining). On the other hand, although direct retail stores mean better services and higher profit margins, the early-stage input costs are huge and take time.

This can also explain why the news of this cooperation was announced by JCPenney or understood in other ways. In this cooperation, JCPenney's need for Nike is far greater than Nike's need for JCPenney.

John Tighe, JCPenney’s chief merchandise officer, said in an interview with the media that they are optimistic about the demand for sports goods brought about by the prevailing sports wind and believe that the establishment of a Nike store in the store will stimulate passenger flow.

This positive view was verified by the competitor Kohl's. Throughout 2015, Kohl's overall revenue increased slightly by 0.9%, with sales of sports and health-related products increasing by 15% year-on-year, which also led the department store to aggressively expand its sports product category (including the introduction of Under Armour). They expect that the sports category will eventually contribute 20% (about $4 billion) of annual sales to the company.

Another reason JCPenney is looking at Nike shop stores comes from their partnership with Sephora in 2006. At that time, JCPenney took Sephora into approximately 600 stores and completely retained the design of the Sephora independent store to achieve the "shop-in-shop" effect. According to a set of figures released by JCPenney last year, Sephora’s department store area has a US$600 annual ping, which is more than three times the average annual sales of the department store.

JCPenney CEO Marvin Ellison stated at the analyst meeting last November that "Sepran's success and its uniqueness lies in expanding the number of JCPenney's products and also making some competitive industry-leading brands part of our supply of goods. "He thinks this has increased JCPenney's competitiveness in the industry." Today, Nike shop-in-shop, with its "product line size expansion," is also seen as a bargaining chip to increase JCPenney's competitiveness.

From the perspective of the entire industry trend, cases of brands entering the department store in the form of “store-in-shop†(rather than regular counters) are appearing more and more frequently. E-commerce firm Rent the Runway recently opened a section of Neiman Marcus, a high-end department store in San Francisco, and another department store, Nordstrom, is running a monthly update of the flash shop series. Olivia, the creative vice president of Open Ceremony Kim acts as a "curator."

In these examples, the supplier (namely, the brand name of the product) is considered to be the “needed†party. This state of “brand power is stronger than the department store†was unthinkable in the past. You know, the "light luxury" brands including Kate Spade, Michael Michael Kors, and Coach all rely on the department store's strong sales network to reach out to the vast majority of consumers. This is also the case with Nike - it encountered supply and demand in 1973. The problem, the solution at the time, was to sign orders with retailers that were "not returned," but offered a 7% discount, and used the department store's network to sell the goods to all parts of the country.

However, a Nike may be difficult to really change the fate of JCPenney. Take Sephora for example. It looks exciting and has improved the effectiveness. However, the fact that Sephora's ping effectiveness is much higher than that of other regions shows that Sephora's efficiency in passenger flow conversion is not that high.

Topics from Pexels.com

Reprinted from: Curiosity Daily

The product is made of food-grade PP material, which is anti-bacterial, insect-proof and not easy to damp. It can be licked and has no peculiar smell. A bowl is double-purpose, can hold water or grain, save time and effort, convenient and practical. The inside of the bowl is professionally polished, the arc does not leave a dead corner, and it is clean after a punch.

Capsule Wiggle Dog Bowl,Slow Feeder Puppy Bowl,Anti Spill Dog Bowl,Dog Bowls For Small Dog

DongGuan Lucky Pet Products Co., Ltd. , https://www.dgpetproduct.com